But the really interesting aspect here is the rationale that SCOTUS used, and the resulting impact for you and me. I went through some of Chief Justice John Roberts comments (note that these are only his opinions and not necessarily representative of all the judges) to gain a further understanding of the ruling:

"The Anti-Injunction

Act provides that “no suit for the purpose of restraining the assessment or

collection of any tax shall be maintained in any court by any person,” 26 U. S.

C. §7421(a), so that those subject to a tax must first pay it and then sue for

a refund. The present challenge seeks to restrain the collection of the shared

responsibility payment from those who do not comply with the individual

mandate. But Congress did not intend the payment to be treated as a “tax” for

purposes of the Anti-Injunction Act. The Affordable Care Act describes the

payment as a “penalty,” not a “tax.” That label cannot control whether the

payment is a tax for purposes of the Constitution, but it does determine the

application of the Anti-Injunction Act. The Anti-Injunction Act therefore does

not bar this suit."

"The Framers knew the difference

between doing something and doing nothing. They gave Congress the power to

regulate commerce, not to compel it. Ignoring that distinction would undermine

the principle that the Federal Government is a government of limited and

enumerated powers. The individual mandate thus cannot be sustained under

Congress’s power to “regulate Commerce.”

In English, Congress does NOT have the power to create commerce, and if you view the ACA in this light, the individual mandate is certainly illegal. In a democratic and capitalistic society, government should not be the one deciding what businesses should be taken and which shouldn't. The market expected the individual mandate in the law to be struck down because of this very argument. BUT, Roberts argues that, although Congress does not explicitly state it as such, the ACA is really a TAX and not forcing commerce. A grey area for sure, but that's how he looks at it.

This is good to know, though. Next time I file my taxes, I'm going to sue the IRS using the opposite argument - forcing me to pay taxes IS forcing commerce as it's supporting the H&R Blocks of the world. I'll let you know how it goes.

"(c) Even if the mandate may reasonably be characterized as a

tax, it must still comply with the Direct Tax Clause, which provides:“No

Capitation, or other direct, Tax shall be laid, unless in Proportion to the

Census or Enumeration herein before directed to be taken.” Art. I, §9, cl. 4. A

tax on going without health insurance is not like a capitation or other direct

tax under this Court’s precedents. It therefore need not be apportioned so that

each State pays in proportion to its population."

Even when viewing it as a tax, the law must be reasonably applied, which the ACA is. So we're good there.

"(b) Section 1396c gives the Secretary

of Health and Human Services the authority to penalize States that choose not

to participate in the Medicaid expansion by taking away their existing Medicaid

funding. 42 U. S. C. §1396c...A State could hardly anticipate

that Congress’s reservation of the right to “alter” or “amend” the Medicaid

program included the power to transform it so dramatically. The Medicaid

expansion thus violates the Constitution by threatening States with the loss of

their existing Medicaid funding if they decline to comply with the expansion."

Another part of the law required states to expand Medicaid eligibility to a broader population. The government would help reimburse the cost of this expansion, but if the states chose not to comply, all Medicaid funding would be taken away. Roberts did find this part of the law illegal, but the implications are limited as this will likely get tweaked anyway. They can just take the threat of withdrawing all funding away, and it should be able to stand otherwise.

Implications for You and Me

So, what does the ruling mean for us? The first thing to realize is this is by no means the end of the fight. Gov. Romney has already said that, if elected, his first task will be to repeal the law entirely. Further, now that SCOTUS has referred to ACA as a tax, yesterday WSJ had an interesting article on how the GOP may use certain law-making provisions that allows the senate to make changes to tax law with only 50% majority, and not the 60% usually required. In other words, be ready to hear more about this.

However, as the bill stands right now, you'll see a few changes:

- Medicare Tax Increases - For those making more than $200k/year ($250k for families), they'll have to start paying more into Medicare on their paychecks. They may also have to pay a slightly higher rate on dividend income depending on the situation.

- Cadillac Plans - Higher taxes will be charges on so-called "Cadillac" plans - plans that have generous benefits and are given to higher level executives. The thought here is if you're getting better coverage than the rest of us, you should pay more for it, and that money should help pay for others' coverage. Many companies have already said that this provision may force them to stop offering those plans.

- Indiividual Mandate - The big daddy - if you don't buy insurance either through your employer, exchanges set up by the states, medicaid/medicare, or privately, then, starting in 2014, you will start paying a penalty on your tax refund of $285 or 1% of your income, whichever is greater. By 2016, the penalty is $2085/family or 2.5% of income. This is the "tax" that SCOTUS is referring to.

- Caps of HSA's - There will be official caps on HSA's. Most companies already some sort of cap, but now there will be a $2500 federal limit. There will also be a 20% penalty in misuse of HSA funds. Oh, finally, indoor tanning has already had a tax increase in place.

My Take (Warning: This May Get Political)

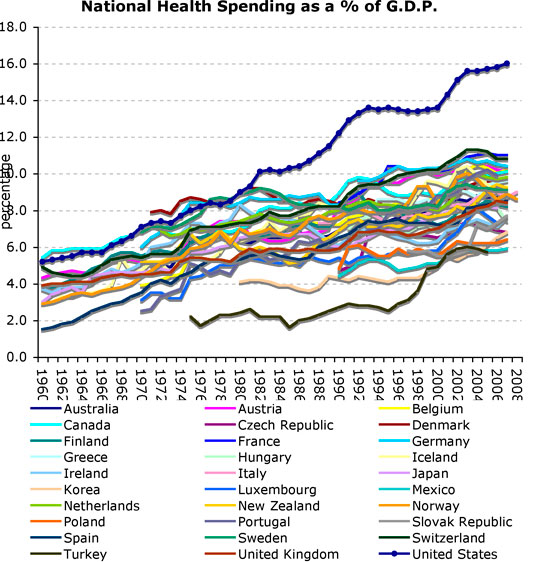

My opinion on this is simple. The US Healthcare system is broken. If you don't believe me, then just look at the two charts to the right (Source: OECD/NYT). If you still don't believe me, then please call me, I'd love to hear your reasons. Therefore, something needs to be done. Now, the key is that whatever is done needs to be over-arching. It has to fundamentally change how healthcare is administered. Some things are already happening - many providers and payer are focusing on reimbursing for 'outcomes' and not 'procedures', and, although I feel that this is important, it will take time. Regulations can help speed the process along. A perfect example of this is the MLR requirements in the ACA. MLR (medical loss ratios) is the percentage of every premium dollars that is spent on paying claims. In the ACA, there is a minimum limit for the (roughly 80-85%). Although on the surface it may seem as odd, I think it will have an interesting impact on managed care companies - it will force them to focus more on their operational efficiency and manage overhead costs much more closely. This is something that I feel managed care companies have done poorly and has resulted in inflated costs for everyone.

My opinion on this is simple. The US Healthcare system is broken. If you don't believe me, then just look at the two charts to the right (Source: OECD/NYT). If you still don't believe me, then please call me, I'd love to hear your reasons. Therefore, something needs to be done. Now, the key is that whatever is done needs to be over-arching. It has to fundamentally change how healthcare is administered. Some things are already happening - many providers and payer are focusing on reimbursing for 'outcomes' and not 'procedures', and, although I feel that this is important, it will take time. Regulations can help speed the process along. A perfect example of this is the MLR requirements in the ACA. MLR (medical loss ratios) is the percentage of every premium dollars that is spent on paying claims. In the ACA, there is a minimum limit for the (roughly 80-85%). Although on the surface it may seem as odd, I think it will have an interesting impact on managed care companies - it will force them to focus more on their operational efficiency and manage overhead costs much more closely. This is something that I feel managed care companies have done poorly and has resulted in inflated costs for everyone. So now that I've established the problem, the next question is what is a potential solution. The ACA is by no means perfect (I have my doubts on how these health exchanges will work depending on how they're executed). But the fundamental risk management strategy for health insurance needs to change so companies can better serve their members at reasonable cost without leaving some out in the cold and still being profitable. It's a tough balancing act, but the individual mandate tries to directly solve this in a sensible way (again, it needs to be over-arching, and that's what this is). Are there better solutions out there? I'm sure there are. Have I seen any proposed? No. So those running around yelling and screaming that this law is bad and will repeal it are basically saying either "there's a problem, I don't have a solution, so I'd rather just ignore it than use one that may work" or (even worse) "I refuse to admit there's a problem at all." That, to me, is just ludicrous.

So now that I've established the problem, the next question is what is a potential solution. The ACA is by no means perfect (I have my doubts on how these health exchanges will work depending on how they're executed). But the fundamental risk management strategy for health insurance needs to change so companies can better serve their members at reasonable cost without leaving some out in the cold and still being profitable. It's a tough balancing act, but the individual mandate tries to directly solve this in a sensible way (again, it needs to be over-arching, and that's what this is). Are there better solutions out there? I'm sure there are. Have I seen any proposed? No. So those running around yelling and screaming that this law is bad and will repeal it are basically saying either "there's a problem, I don't have a solution, so I'd rather just ignore it than use one that may work" or (even worse) "I refuse to admit there's a problem at all." That, to me, is just ludicrous.

I'll also add that the current political climate just reinforces this argument. Politicians right now just don't get it. They seem to think that sticking to their bases and moving more to the left or the right is what the country needs. The national debt ceiling debacle last year was a perfect example of this. What they don't understand is that people elect them for a more important reason - to actually get things done. Instead of coming together and making compromises, they choose to move apart, and if ACA does get repealed, the chances of something else getting passed is next to zero. Again, the problem will still be there, and nothing will be done about it.

So, do I like ACA? It's a solid attempt at fixing an issue, yet it has some flaws. But those flaws are not nearly severe enough to go back to square one. That is the most dangerous scenario out there.

PS - I didn't use this in my argument anywhere, but I found this chart interesting (from the Washington Post). Even if you consider the entire ACA a tax, the size of it is actually not as large as some GOP'ers are describing them to be.

What are your thoughts?

Questions/Comments/Feedback? Please don't hesitate to let me know. Suggestions on posts you'd like to see? Let me know!

The Standard Disclaimer:

Everything I've written above is my opinion and my opinion only. Please do not take it as fact. Perform all necessary due diligence prior to acting on any recommendations, including consulting a financial adviser.

Questions/Comments/Feedback? Please don't hesitate to let me know. Suggestions on posts you'd like to see? Let me know!

The Standard Disclaimer:

Everything I've written above is my opinion and my opinion only. Please do not take it as fact. Perform all necessary due diligence prior to acting on any recommendations, including consulting a financial adviser.

No comments:

Post a Comment